Open Banking: How Australia can learn from the UK

Posted by

Sandstone Technology on Nov 24, 2020 9:02:01 PM

Topics: Digital Banking, Data & Open Banking

Open Banking drew global attention in 2016 as a direct result of the UK’s Competitions Market Authority announcing plans for the top 9 banks in the UK to deliver open source Application Programming Interfaces (APIs) for 3rd party use by January 2018.

Since then, Open Banking has been introduced in many countries around the world with varying regulatory and standardisation controls. In the UK the regulatory framework and cost of entry has seen significant shortcomings in the uptake of Open Banking.

Here in Australia, the government announced a review into Open Banking as part of 2017 Federal Budget. Open Banking legislation passed in August 2019. We should not be looking at the UK experience as one which will be replicated as there exists significant differences between the two markets which will see Australian banks and Financial Institutions approach Open Banking with a shift in mindset.

In Australia, payments are not part of the regulatory framework as the focus has been only on read access to the data.

A consistent authentication flow has been adopted by the Consumer Data Right (CDR) which requires a One Time Password (OTP) to be delivered to the consumer through existing and preferred channels. Strong Customer Authentication (SCA) in the UK has placed restrictions on banks and inhibited the customer experience.

The Open Banking Directory (OBD) in the UK regulates third party providers and account providers that operate in the Open Banking ecosystem. Regulated third party providers manage the digital certificates and software statements needed to connect to account providers using the Open Banking API Standards. In Australia, the Competition and Consumer Commission (ACCC) will

perform the role of the CDR Registrar. The CDR Registrar will maintain the Register of Accredited Persons (the Register) who have been accredited by the ACCC in its capacity as Data Recipient Accreditor. The ACCC Certificate Authority (CA), DigiCert, will issue and manage certificates to CDR participants as directed by the ACCC in its capacity as the CDR Registrar.

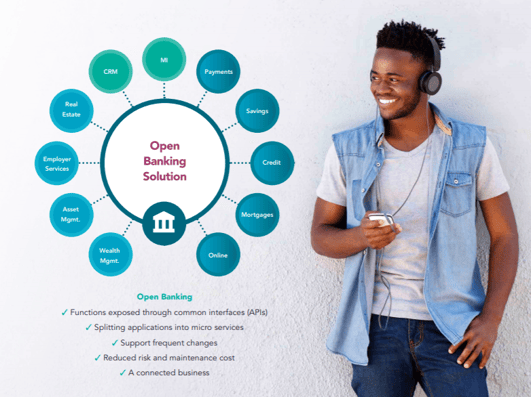

services that can be more efficiently used, both internally and externally.

services that can be more efficiently used, both internally and externally.Open Banking is a concept known in the Fintech industry as “Everything as a service” (XaaS), which is a design approach that enables software to expose its functions to other software, so that a business can operate more efficiently. This software design approach typically results in Application Programming Interfaces (APIs).

The potential benefits of Open Banking include:Despite the unlocked potential of Open Banking, adoption rates are still low. In the UK only 15% of banks have enrolled onto the UK Open Banking directory.

A banks lack of interest in Open Banking can be attributed to several different factors however the three main drivers have been regulation, complexity and fear.

Governments around the world, recognising that financial data belongs to the individual and not the bank, have started introducing legislation to force banks to provide their services externally to authorised third party providers (3PPs). In the EU it was PSD2 and the legislation was known as common secure communication. It focuses on providing both account information and payment services for payment accounts. In some countries, regulation encompasses more account types but focuses solely on account information. Many have labelled this legislation as Open Banking and it has unfortunately stuck.